If the bond market sounds abstract, intimidating, or like something only bankers need to worry about, you’re not alone. Most people never encounter it directly. You can live your whole life without buying a bond, reading a yield chart, or watching a gilt auction.

And yet the bond market shapes:

- how much your government can spend

- how much tax you pay

- the state of public services

- the cost of your mortgage

- the stability of the economy

- and the limits of every political promise you hear

It is the quiet force behind the curtain – the one that doesn’t appear on ballot papers but still influences the outcome of every government’s plans.

So let’s break it down, simply and honestly.

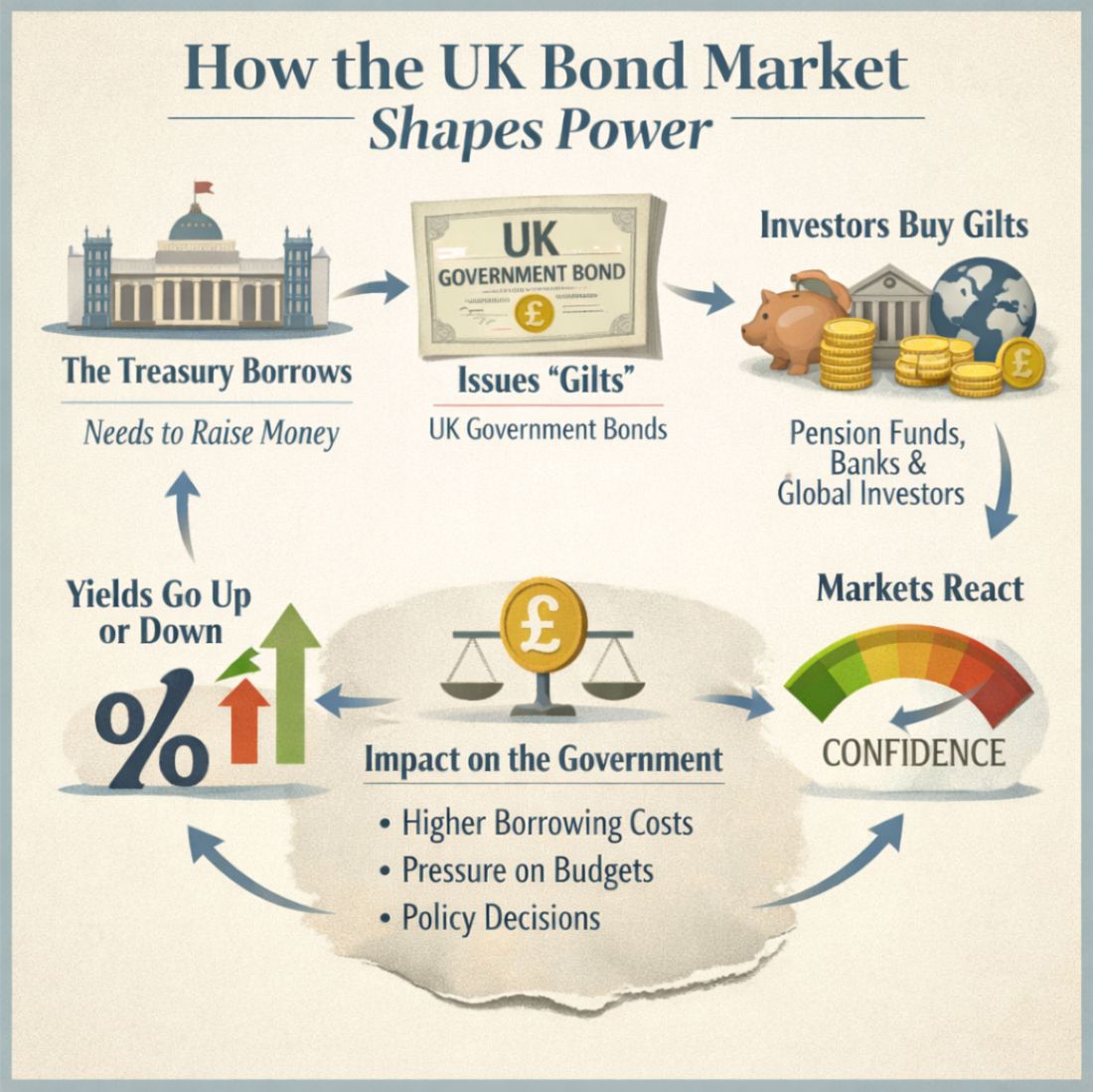

What is the bond market?

Imagine the government needs money – not for a rainy day, but for everything from schools to pensions to defence to the NHS. Taxes cover some of it, but not all. The gap between what the government spends and what it collects is filled by borrowing.

To borrow, the government issues bonds – IOUs that promise to pay interest over time.

These bonds are bought by:

- pension funds

- insurance companies

- banks

- investment firms

- foreign governments

- and large institutional investors

They buy bonds because they want a safe place to store money and earn a predictable return.

In other words:

The bond market is the place where governments borrow the money they need to function.

Why does the bond market matter so much?

Because the government depends on it.

If investors trust the government, they lend cheaply.

If they lose trust, they demand higher interest – or stop lending altogether.

This is why the bond market is often described as the “referee” of government behaviour. It doesn’t shout. It doesn’t campaign. It doesn’t issue statements. It simply reacts.

And its reactions have consequences.

What happens when the bond market gets nervous?

When investors worry that a government is spending too much, taxing too little, or losing control of the economy, they sell its bonds.

When they sell, the price of bonds falls.

When the price falls, the interest rate (the “yield”) rises.

When yields rise, government borrowing becomes more expensive.

This is not a gentle nudge.

It is a financial shockwave.

Higher borrowing costs mean:

- less money for public services

- more money spent on debt interest

- pressure to raise taxes

- pressure to cut spending

- and a shrinking ability to invest in anything new

This is exactly what happened during the Liz Truss mini‑budget.

The markets didn’t “punish” her. They simply lost confidence – and reacted automatically.

Why can’t governments just ignore the markets?

Because the way government works today means that it needs to borrow constantly.

Not once a year.

Not once a decade.

Every single week.

The UK rolls over old debt and issues new debt continuously. If investors stop buying, the government cannot fund itself.

This is why no government – left, right, or centre – can simply “tell the markets to fall in line.”

It would be like telling your bank manager that you don’t feel like paying interest anymore.

The system doesn’t work that way.

Why does this feel so disconnected from everyday life?

Because the bond market operates in a world most people never see.

When you hear politicians talk about “growth,” “fiscal rules,” or “market confidence,” they are speaking to this invisible audience – not to the public.

And when they talk about “growth,” they mean GDP, not the kind of growth people actually feel in their lives.

GDP can rise while:

- wages stagnate

- services decline

- inequality widens

- and communities fall apart

So when politicians celebrate “growth,” they are often signalling to the markets that the system is still functioning – not announcing that life is about to get better.

This is why the public hears optimism while politicians feel fear.

So who really holds the power?

Not in a conspiratorial sense – but in a structural one:

The bond market holds more power over government spending than any manifesto ever written.

It doesn’t care who wins elections.

It doesn’t care about ideology.

It doesn’t care about promises.

It cares about one thing:

Whether the government looks like a safe bet.

If it does, borrowing stays cheap.

If it doesn’t, the system tightens like a vice.

Why does this matter now?

Because Britain’s fiscal position is fragile:

- debt is high

- interest costs are rising

- public services are stretched

- productivity is weak

- and the economy is heavily dependent on imported energy and goods

This means the next government – any government – will face extremely limited room for manoeuvre.

Not because they lack ideas.

Not because they lack ambition.

But because the system they inherit is already at its limits.

The uncomfortable truth

The bond market is not the enemy.

But it is not a neutral observer either.

It is the mechanism through which decades of political decisions – outsourcing, deregulation, financialisation, and dependence on debt – have come home to roost.

And until the public understands how this system works, the gap between political promises and political reality will continue to widen.

Because the truth is simple:

The bond market doesn’t take orders.

It sets the boundaries within which politics now operates.

And any politician who cannot explain that – or refuses to – is not being honest about the world we live in.