A World That Teaches Us to Blame Ourselves

We live in a world where many people quietly carry guilt for failing at dreams they never truly chose.

They look at their lives, see the gap between expectation and reality, and assume the fault must lie within themselves. They believe they lacked discipline, talent, intelligence, resilience, or worth.

But they are not responsible for the dreams they were handed.

They didn’t design the system that shaped them.

They didn’t choose the story they were born into.

The only “mistake” they made – if it can even be called that – was believing a narrative so compelling, so omnipresent, that resisting it felt impossible.

This essay is about that gap: the space between the life people were promised and the life the modern system made possible. It looks at education, work, housing, relationships, community, and faith not as separate problems, but as parts of the same story.

The Story We Inherit

From childhood, we are taught that we are small parts of something vast: society, the economy, the world order.

We are told that the world is too big, too complex, and too specialised for ordinary people to understand. We are encouraged to trust the experts, leaders, institutions, and systems that claim to know better.

And so we do.

We accept the roles we are given.

We chase the dreams placed in front of us.

We measure ourselves against standards we never agreed to.

When those dreams break, we assume we broke them.

But the truth is far simpler:

We are living inside a story written by others.

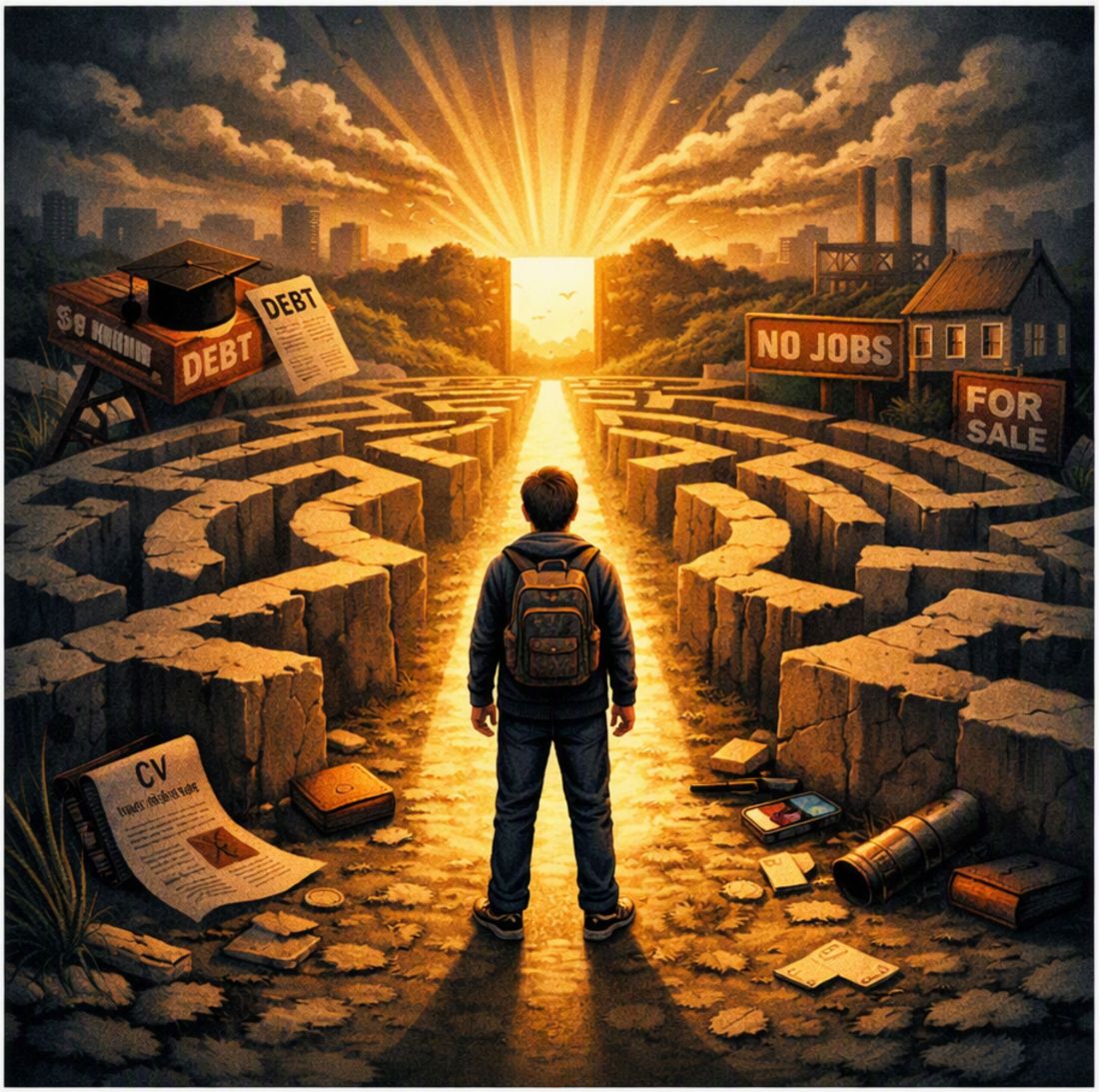

A Concrete Example: The University Dream

Nowhere is this clearer than in the story told to young people about their future.

For decades, young people have been encouraged – and often pressured – to believe that a bright future begins with university.

They are told that higher education is the gateway to success, stability, and opportunity. They are warned that without a degree, they will fall behind.

But many of these young people are not suited to that pathway.

And worse, the pathway that would suit them often doesn’t exist.

So they follow the script:

- They take on debt to study courses that no employer needs.

- They graduate into industries that never promised them a place.

- They discover that the “glittering career” they were sold doesn’t exist.

- They end up in minimum‑wage jobs that cannot support independent living.

- They face the spectre of rising debt they can never realistically repay.

And then – heartbreakingly – they blame themselves.

They think they failed.

They think they weren’t good enough.

They think they made bad choices.

But the truth is this:

They were following someone else’s dream – a dream designed by a system that needed them to believe in it.

This is what a broken dream looks like: not a personal failure, but a structural one.

How the System Removed the Pathways That Once Worked

The tragedy runs deeper than individual disappointment. Over the past few decades, the system has quietly removed many of the circumstances, opportunities, and pathways that once allowed ordinary people to build meaningful lives.

This didn’t happen because traditional jobs “couldn’t be monetised.”

It happened because the pursuit of profit and market dominance made their removal more valuable than their preservation.

When globalisation, deregulation, and financialisation took hold, the priority became:

- lowering labour costs

- increasing shareholder returns

- consolidating market power

- maximising efficiency

- expanding corporate reach

And in that pursuit, the system dismantled the foundations of community‑rooted work.

There was a time when young people who weren’t academic – or simply weren’t ready for academia – could enter the world through apprenticeships, trades, local industries, and community‑based jobs.

These pathways offered:

- dignity

- identity

- belonging

- progression

- stability

- contribution

- purpose

But these jobs required long-term investment in people, places, and skills. They created strong communities, and strong communities are harder to control. They produced independence, and independence is harder to monetise indirectly.

So they were moved offshore, automated, consolidated, or eliminated.

Not because they lacked value, but because their destruction generated more value for the system than their continuation.

The experiential route – the one that shaped generations – collapsed under the weight of market logic.

And with those pathways gone, millions of young people were funnelled into the only route the system still recognised: university. Not because it suited them, but because it was measurable, monetisable, and profitable.

The result is a generation carrying debt for qualifications employers do not always need, working in jobs that often do not pay enough to live independently, while believing they failed – when in truth, the system removed many of the alternatives.

And once work no longer guarantees security, the consequences spread into every other part of life.

What a Real Life Once Looked Like

Before the system reshaped everything around extraction and efficiency, a working life offered something simple and profound: enough.

Working a normal week once meant:

- your needs were met

- you had independence

- you had dignity

- you had a place in your community

- you had peace

It wasn’t glamorous.

It wasn’t excessive.

It wasn’t designed to impress anyone.

But it was enough – and enough was a life worth having.

People did not need to chase endless growth, endless consumption, or endless status.

They did not need to “keep up.” They did not need to perform success. They simply lived, contributed, and belonged.

And the irony – the painful irony – is that many who defend the current system will scoff at this. They will dismiss that kind of life as inadequate, small, or unambitious. They will insist that “people should want more.”

But these are often the same people who are constantly chasing an ever-moving baseline – the invisible line between those who are “keeping up” and those who are being left behind. That line shifts every year, ensuring that nobody ever truly arrives.

The tragedy is that the life they dismiss is the life most people are quietly longing for.

A life where work provides stability, not anxiety.

A life where independence is possible without debt.

A life where value isn’t measured in consumption.

A life where peace isn’t a luxury.

This is what the system took away – not by accident, but because an extractive economy cannot profit from people who already have enough.

This pressure to perform a successful life does not stop at work or money. It reaches into the way people love, commit, and choose partners.

The Relationship Trap

The same forces that reshaped work and opportunity have also reshaped relationships.

Many young people now feel pressure to conform to a relationship ideal that has less to do with genuine connection and more to do with external validation.

They are encouraged to see relationships as:

- a marker of adulthood

- a symbol of stability

- a sign of social success

- something that “looks right” to others

And because so many grow up without the social grounding that once came from community life, they often enter relationships without the skills, experience, or self‑knowledge that previous generations absorbed naturally.

For most of human history, young people learned how to understand others – and themselves – through osmosis:

- in extended families

- in neighbourhoods

- in intergenerational communities

- in shared public spaces

- in workplaces where people mixed across ages and backgrounds

These environments taught subtle but essential skills:

- reading intentions

- recognising values

- understanding boundaries

- navigating conflict

- spotting red flags

- knowing what compatibility actually means

Today, those environments have collapsed.

Young people now learn about relationships from:

- distant sources

- digital platforms

- curated personas

- algorithmic feeds

- entertainment built on fantasy

These sources cannot teach the realities of human connection.

So when someone appears to “tick the boxes,” many people compromise themselves – not out of weakness, but out of conditioning. They choose relationships based on how they look, how they appear to others, and how neatly they fit the script.

And only later – sometimes years later – do they awaken to who they really are.

By then, the cost can be enormous:

- relationship breakdown

- divorce

- emotional fallout

- or staying in a relationship they should never have been in, out of duty or fear

This is another broken dream.

Not because people failed, but because they were never taught the skills that make relationships work.

The same pattern appears again in housing: a basic human need turned into a test of individual worth.

The Housing Illusion

Housing, one of the most basic human needs, has been transformed into one of the most aggressively monetised assets in the modern economy.

What should be a foundation for stability has become a vehicle for speculation, investment, and wealth extraction.

This shift didn’t happen because people suddenly needed more space. It happened because the financial system discovered that housing could be used to generate enormous returns – not for the people who live in homes, but for the people who treat them as assets.

As a result:

- house prices have expanded far beyond what any normal person can keep up with

- wages have not kept pace

- the cost of entry has become prohibitive

- and the dream of home ownership has drifted out of reach

Not because people failed.

But because the system changed the rules.

Housing is now one of the key performers in the economic model we live under. Rising house prices inflate GDP, fuel lending, and enrich those who benefit from asset inflation.

And the irony is brutal:

People don’t need more than one home to live in.

But the system rewards those who collect homes, not those who need one.

The people who need the security of a home most are the very people the system refuses to lend to. Meanwhile, those who already have assets are given the loans, the leverage, and the opportunities to profit from the very people who are locked out.

So the people with the least security are placed at the mercy of those who have the most.

This increasingly looks less like a natural market outcome and more like a structural design.

And once again, people blame themselves for failing to achieve a dream that was quietly taken away.

Once people are priced out of security, they are told to prove themselves harder. This is where the myth of meritocracy becomes so powerful.

The Meritocracy Myth

Another broken dream – perhaps the most quietly corrosive of all – is the idea of meritocracy.

People are told that success comes from talent, hard work, and personal merit. But in practice, meritocracy rewards something very different: conformity.

To “get on,” people must:

- follow the academic route

- accumulate credentials

- demonstrate compliance

- avoid asking uncomfortable questions

- fit neatly into the expectations of the system

This isn’t merit.

It’s alignment.

Because the system defines merit through measurable outputs – grades, salaries, promotions, performance metrics – people are pushed into a lifelong cycle of proving themselves through numbers that never stop moving.

On one side, they must earn more just to keep up with rising costs.

On the other, the real value of their earnings keeps falling.

So they run faster, work harder, and sacrifice more – not to get ahead, but simply to avoid falling behind.

And the people who “succeed” in this system are often those who have learned not to question it. They rise by saying yes, by fitting the mould, by demonstrating reliability through compliance rather than insight.

This is how we end up with a managerial class that can confuse management with leadership: people trained to defer to systems, specialists, and advisers, sometimes without understanding the human realities beneath the decisions they make.

This isn’t a failure of individuals.

It’s the predictable outcome of a system that rewards conformity over clarity, compliance over courage, and credentials over competence.

Yet beneath education, work, housing, and status lies something even deeper: the loss of community itself.

The Collapse of Community

Perhaps the greatest tragedy of all is the collapse of community – the quiet erosion of the environments that once taught people who they were, how to live, and what truly mattered.

For most of human history, community wasn’t an optional extra.

It was the structure that shaped identity, belonging, and meaning.

It taught people:

- how to relate

- how to contribute

- how to resolve conflict

- how to care

- how to be seen

- how to be human

These lessons weren’t taught formally.

They were absorbed through osmosis – in shared spaces, intergenerational relationships, and the natural rhythms of communal life.

But as the modern system reorganised itself around money, efficiency, and individual performance, community became an inconvenience.

It could not easily be monetised. It could not easily be measured. It could not easily be turned into a product.

So it was allowed to wither.

People have been encouraged to see themselves as isolated units – consumers, workers, individuals – rather than members of a shared life.

The narratives shifted from:

“We belong to each other”

to

“You’re on your own.”

And in that shift, something essential was lost.

We are being conditioned to forget who we really are and what a life with value actually looks like.

A life built on:

- people

- relationships

- shared purpose

- mutual support

- place

- belonging

Instead, we are told that value comes from money – and from everything the narratives claim money can do for us.

But money cannot replace community.

It cannot teach empathy.

It cannot create belonging.

It cannot give identity.

It cannot provide meaning.

It cannot hold you when life breaks.

It cannot teach you how to live.

Community once offered all of this freely.

It was the most effective, cost‑free training for life that anyone could have.

In a world where everything is expected to pay its way, community has been replaced by distant, digital, and commercial substitutes that cannot fully understand the realities of the lives people actually face.

And without community, people lose the mirror that once reflected their worth back to them. They lose the grounding that once told them who they were. They lose the sense of shared humanity that once made life feel meaningful.

This is not a small loss.

It is the collapse of the foundation on which everything else depends.

When community collapses, so does the inner space where reflection, meaning, and faith can take root.

The Collapse of Faith Capacity

This erosion of inner space has consequences far beyond work and opportunity. It may also help explain why institutions such as the Church of England are struggling to hold the attention and trust of modern life.

Faith – in any tradition – requires:

- reflection

- stillness

- imagination

- contemplation

- humility

- a sense of the transcendent

- the ability to hold ideas that cannot be measured

These are the exact capacities the modern system has stripped away.

People today are:

- overstimulated

- overworked

- financially stressed

- time‑poor

- mentally fragmented

- constantly distracted

- conditioned to think only in measurable terms

Faith is unmeasurable.

Meaning is unmeasurable.

Purpose is unmeasurable.

So the system quietly teaches people to dismiss them – not because they are unimportant, but because they cannot be monetised.

The collapse of faith is not a failure of people.

It is a symptom of the same structural forces that created the world of broken dreams.

Some will argue that modern systems have also brought genuine progress: longer lives, wider education, greater mobility, and opportunities previous generations did not have.

All of that is true. But the question is not whether progress exists. The question is what kind of life that progress has left ordinary people able to live, and what has been lost along the way.

If the old dream is broken, then the answer cannot simply be to try harder inside it. It must be to remember what a human life actually needs: meaningful work, secure shelter, honest relationships, living community, inner stillness, and the freedom to trust one’s own direction.

The Truth We Were Never Taught

The truth is not that we are small.

The truth is not that we must fit into the world as it is.

The truth is not that we must earn permission to be ourselves.

The truth is this:

Your inner guidance is enough.

It always was.

You are already big enough for the life you are meant to live.

You do not need validation from the system.

You do not need permission from society.

You do not need to justify your existence by meeting inherited expectations.

You only need to reconnect with the part of you that the system taught you to ignore – and then begin rebuilding life from that place.

That does not mean retreating from the world. It means seeing the world clearly enough to choose differently within it: to value enough over excess, belonging over status, contribution over performance, and truth over approval.

Reclaiming What Was Always Yours

When you stop blaming yourself, something extraordinary happens:

- You stop feeling guilty for failing at someone else’s dream.

- You stop apologising for wanting something different.

- You stop shrinking to make others comfortable.

- You stop mistaking conditioning for truth.

- You stop believing you are smaller than you are.

And then, for the first time, you begin to see the world clearly.

You realise that independence isn’t arrogance.

Self‑trust isn’t delusion.

Inner guidance isn’t naïve.

It is the most natural thing in the world.

It is the thing you were born with.

The thing you were taught to forget.

The thing that will not make the old dreams yours – but may finally help you build a life that is.